Stocks and bonds serve as a means for investors to preserve or increase the value of today for the future, embodying contracts between investors and companies in a securitized form. The ability to sell these securities as needed provides greater liquidity.

Stock exchanges play a crucial role in providing such liquidity to investors. Another important function of exchanges is to monitor and evaluate companies. Investors, armed with information about a company’s health and performance from various sources, make their own judgments on the value of a company. If investors collectively decide that a company’s management is performing poorly, the selling pressure can drive down the stock price, effectively allowing investors to supervise the company and granting them freedom.

The age of exploration led by Columbus’s westward voyages, transitioning into the age of merchants, significantly contributed to the development of finance, initially taking root in the Netherlands, Europe. Late to the competitive maritime trade, the Netherlands established the Dutch East India Company as a joint-stock company in 1602. The world’s first stock exchange appeared in Amsterdam in 1609 to trade these stocks, and the first bank was established to facilitate capital flows. This exchange traded not only Dutch East India Company stocks but also government bonds, attracting Dutch officials, the elite, their servants, and foreign nobles.

Stock exchanges and banks brought together those in need of capital and those who had it. This allowed multiple investors to share risks and pool large sums of money, enabling the pursuit of larger and riskier ventures. This advanced financial system gave Dutch merchants a competitive edge. It’s no coincidence that New York, the financial hub of today, was originally New Amsterdam, established by the Dutch.

However, as the world’s economic power shifted to Britain, so did the center of the financial industry. The development of Britain’s financial markets was based on the Industrial Revolution, but interestingly, the financial industry itself started in coffeehouses. Opening around 1602, these coffeehouses soon became places for business and information exchange, drawing people to share news and money. This led to the informal stock exchange that began around 1773, eventually leading to the official establishment of the London Stock Exchange in 1801. London then became the center of the global financial industry.

Following World War I, as the American economy flourished, the U.S. began to compete with Britain in the financial sector, eventually dominating the global economy after World War II. As U.S. manufacturing moved to emerging Asian countries, the U.S. started to develop its financial industry as a new engine of national growth. The deregulation of the financial industry in the mid-1970s led to the emergence of various derivatives and hedge funds, marking the beginning of the era of U.S. investment banks.

As financial markets evolved, products detached from the real economy appeared, and systems promoting transactions for their own sake introduced speculative elements. The uncertainty of the stock market spurred greed to realize future corporate earnings today, leading to bubbles such as the Black Monday of 1987 and the collapse of the dot-com bubble in 1990.

The stock market, investing in company stocks and bonds, once played a crucial role in elevating individuals to the middle class and using their savings to grow companies. However, the market has since been dominated by derivatives unrelated to companies, introducing short selling and margin trading, transforming it into a speculative gambling arena. It’s no longer a place for individuals with savings or investment objectives but a zero-sum game that divides people into winners who make a fortune and losers who squander their wealth.

However, the emergence of speculative and gambling elements is not a recent phenomenon. Bubbles are inherently born from uncertainty.

A prime example of a bubble born from uncertainty occurred in the Netherlands, where the financial system first developed. When the first ship of the Dutch East India Company set sail in 1604, its stock price rose by more than 30% compared to its 1602 issuance. Rumors of shipwrecks or pirate attacks could cause stock prices to plummet overnight, but during good economic times, prices could skyrocket tenfold.

Seeing the potential to make money from stocks, the Dutch began to speculate on other items, including tulip bulbs. Imported from Turkey, tulips were highly valued by Europeans, leading to a rapid increase in demand. Anticipating continued growth in tulip demand, merchants began buying future harvests of tulip bulbs, essentially engaging in futures trading. This attracted investment from the upper class and even their servants.

As the entire nation and foreigners dove into tulip speculation, the Amsterdam stock exchange listed tulips for trading, similar to how ratings are assigned to U.S. subprime bonds. However, unlike stocks, no one could predict the color of tulips that would bloom from the bulbs, making it all a manipulation. It was later discovered that tulip colors were determined by virus infections.

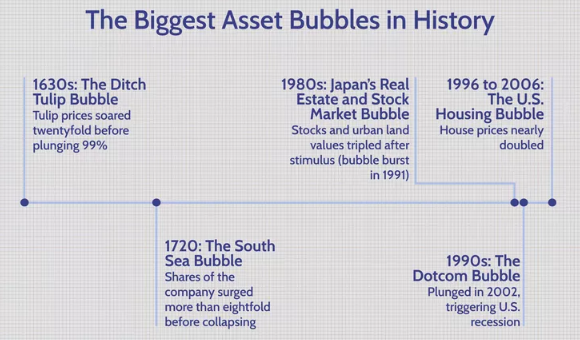

But if a tulip bulb were to sprout a Semper Augustus, it could indeed make a tremendous amount of money. This was because a single tulip bulb could be worth as much as a large mansion. Such irrationality created an unimaginable bubble in tulip prices. Moreover, unlike stocks, tulip bulbs were tangible items that could be seen with the eyes. Not just nobles and merchants, but also farmers and maids were all swept up in the speculative fever. This tulip frenzy continued for three years. Then, one day in 1637, some people realized they could not sell the tulip bulbs at the high prices they had anticipated. As uncertainty over how high the prices could go turned to panic, the price of tulip bulbs, which had been soaring, plummeted overnight, recording a 95-99% drop in just four months. Only then did people realize that tulip bulbs were of no use except for planting in gardens, but by then it was too late.

The growth of Europe’s financial industry led to an overflow of capital crossing the Atlantic to America. Manhattan Island, bought from the Indians by the Dutch in 1624, passed to the English and then became part of the United States. Traders and financiers gathered there called it Wall Street, marking the beginning of the world’s largest licensed gambling den.

Investing in stocks means reducing today’s consumption to prepare for the future. From a company’s perspective, it’s debt. However, individual investors are creating debt by taking on debt. Short selling, too, is a system that allows selling stocks one does not own, essentially borrowing stocks. Betting on a stock price drop using borrowed stocks is short selling. Thus, it can no longer be considered an investment. It’s merely a game with money, without any link to the real economy.

Thus, as the financial market drifted away from the real economy, bubbles formed and crises ensued.

:max_bytes(150000):strip_icc()/Dutchtulips-29ea38f5781246a6938879da97eb200f.jpg)