The Widening Gap Between Physical Assets and Finance

Stocks and Bonds: Money Created by Corporations and Financial Institutions

It’s not just governments and banks that create money. Countless corporations, investment banks, and securities firms also pour various types of money into the economy. What if there was no way to store the wealth I save or earn today for tomorrow? The world might have been a more equitable place. Of course, this would come at the cost of economic growth becoming more challenging, as everyone in the global village would only work enough to live for today.

Money allows a portion of today’s production value to be stored for the future. Though it’s hard to imagine now, saving might become a method that requires payment in the future. In fact, some are already paying the cost of storing money through something called inflation.

For now, there are more people wanting to spend money than save it, resulting in a higher cost of use, and ultimately, it’s the users of money who are paying interest. Up to today, there have been more people in the global village wanting to borrow others’ money than those wanting to save. Not all of them are simply looking to spend their expected future income today. Among those in need of money, many have ideas that could produce more efficiently than others. We call these people entrepreneurs.

In the early days of the market economy, individuals would exchange the surplus of goods they produced for those they lacked. However, as commerce became mutually beneficial and specialization continued, people emerged who produced and sold only one type of good. The problem is that production and sales do not happen simultaneously. One must first buy the necessary equipment and raw materials for production.

Entrepreneurs in need of money go to banks to borrow money, making more money circulate in the entire society, but they also issue their own currency. We call the money they issue stocks and bonds. From the company’s perspective, these are liabilities, but for the lender, they are stocks and bonds. These securities are also a type of money. Think of a company’s promissory note. There was a time when it was very natural for a promissory note issued by a company to circulate in the market as money.

Of course, not all money is the same. There are differences primarily in liquidity and uncertainty.

Liquidity relates to how easily it can be exchanged for other assets. For example, with ten thousand won in cash, you can go to the market and buy whatever you want for ten thousand won without additional costs. On the other hand, if you want to buy other property or products with a bond from a listed company, you’d have to visit a securities company or leave it as collateral at a bank to borrow money. All these actions incur costs.

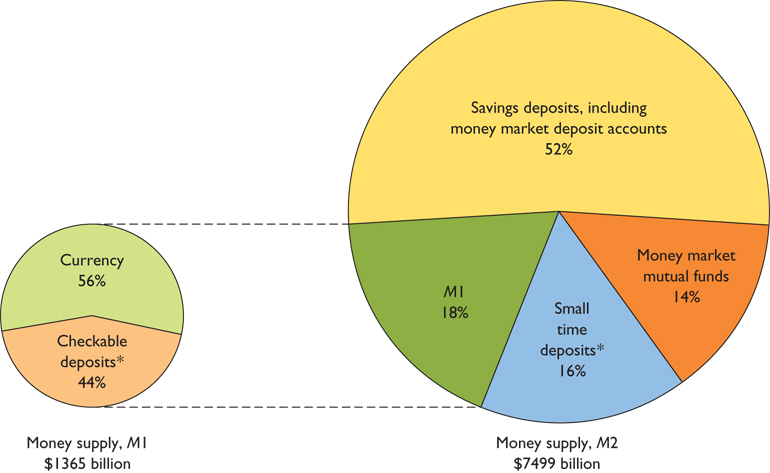

The most liquid form of money is cash issued by the central bank. However, we don’t keep this cash in our home safes. Usually, it is deposited in banks and withdrawn for use as needed. The money that can be easily withdrawn and used in this way, combined with bank deposits, is referred to as M1 in the narrow sense of currency.

Even though liquidity has decreased, money saved in financial institutions for asset growth, such as time deposits, savings accounts, or funds, can also be converted into cash if desired. These financial products can also be considered a broader sense of money because they can be withdrawn in cash anytime if one is willing to forfeit the interest to be received at maturity. Combining this type of money with the more liquid M1 results in M2. When we talk about the money supply, we usually mean M2.

Including securitized debt (Security Debt) and others, we refer to it as L (Liquidity Aggregates) in the broad sense of liquidity indicators. Securitized debt includes national bonds issued by governments but mostly consists of bonds and liquid financial products issued by corporations and various financial institutions. Though liquidity has decreased and uncertainty has increased, these are still forms of money that directly benefit the real economy.

Derivatives: Money Detached from Physical Assets

People are not satisfied with this. They begin creating new debts based on existing ones, generating money that lacks in both liquidity and safety. This is what we call derivative financial products. Derivative securities are securities created based on traditional financial assets like stocks and bonds. The derivatives we occasionally come across, such as futures, options, and swaps, fall into this category.

These derivatives also play a crucial role in economic development, for instance, by providing a means to hedge against risks. The issue is, for someone wanting to avoid risk, there must be another party willing to take on that risk in hopes of making more money. Another significant function is transforming or synthesizing basic commodities to create new financial products, providing an essential service to the economy. For example, when the scale of investment is too large for individuals to directly invest in real estate, shares or bonds related to real estate development can be broken down and sold to small-scale investors. This process offers opportunities to those who cannot directly participate in that market.

Products related to subprime mortgages serve a similar purpose. Derivative financial products, such as Mortgage-Backed Securities (MBS) and Collateralized Debt Obligations (CDO), are created based on long-term housing loans, mortgage loans. These products also represent credit money. If someone wants to buy a house but lacks sufficient funds, they can borrow money from a financial institution to purchase a home. This financial system benefits both construction companies, which can sell houses, and buyers, who can purchase homes despite lacking funds. Of course, the financial institution holds the house as collateral. Up to this point, it’s a simple creditor-debtor issue with the bank. However, the evolution of financial products doesn’t stop there; these debts are used as base products to create new ones, like MBS and CDO. Debt thus becomes another form of credit money, or in other words, money.

The problem arises when credit money becomes increasingly detached from the underlying products and services, making it easier to create malignant bubbles. As it moves further away from the real economy, it might turn into a ‘money-for-nothing’ phenomenon. If such a bubble bursts, the securities, which are nothing but debts, lose their value. Remember, this debt was essentially money.

The disappearance of debt means, ultimately, money vanishes. This money was what drove economic growth. If someone refuses to lend money, credit contracts, and money shrinks and evaporates.

According to a report created in 2006 by Independent Strategy (www.instrategy.com) based on statistics from the Bank for International Settlements in Switzerland, the money issued by governments worldwide accounts for only 1% of all money circulating globally, while money created by banks represents 11%, and money generated for corporate economic activities accounts for 13%. The remaining 75% is attributed to derivative financial products.

In reality, money related to the real economy extends only to securitized debt. Derivative financial products, which sit at the top of the pyramid, represent money unrelated to the real economy. Money exceeding 800% of the global gross production is circulating around the world.